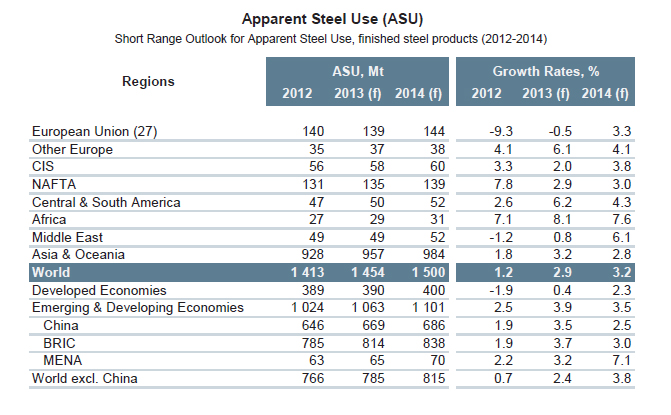

![]() London, 11 April 2013 – The World Steel Association (worldsteel) today released its Short Range Outlook (SRO) for 2013 and 2014. worldsteel forecasts that global apparent steel use will increase by 2.9% to 1,454 Mt in 2013, following growth of 1.2% in 2012. In 2014, it is forecast that world steel demand will grow further by 3.2% and will reach 1,500 Mt.

London, 11 April 2013 – The World Steel Association (worldsteel) today released its Short Range Outlook (SRO) for 2013 and 2014. worldsteel forecasts that global apparent steel use will increase by 2.9% to 1,454 Mt in 2013, following growth of 1.2% in 2012. In 2014, it is forecast that world steel demand will grow further by 3.2% and will reach 1,500 Mt.

The worldsteel Economics Committee met 6-7 April 2013 in Dusseldorf, Germany.

Commenting Hans Jürgen Kerkhoff, Chairman of the worldsteel Economics Committee said, “2012 was a challenging year for the steel industry with apparent steel use increasing at the slowest rate since 2009 when demand declined by -6.5%. This was mainly due to the Eurozone crisis which persisted throughout 2012 and whose impact was felt further afield. On top of this, corrective macroeconomic measures in major emerging economies also contributed to a concerted slowdown globally.

However, in the early part of 2013, the key risks to the global economy – the Eurozone crisis, a hard landing for the Chinese economy, and the US fiscal cliff issue – have all stabilised considerably and we now expect a recovery in global steel demand to kick in by the second half, led by the emerging economies. Yet, the situation on the financial markets remains fragile and the Eurozone crisis is far from being solved as the recent events in Cyprus have again shown.

In 2014, we expect a further pickup in global steel demand with the developed economies increasingly contributing to growth.”

Apparent steel use in China is expected to grow by 3.5% in 2013 to 668.8 Mt following a 1.9% increase in 2012. In 2014, steel demand is expected to grow by 2.5% as the Chinese government’s measures to control investment in an effort to rebalance the economy will remain in place.

In India, steel demand is also expected to pick up and will grow by 5.9% to 75.8 Mt in 2013 following 2.5 % growth in 2012 as monetary easing is expected to support investment activities. In 2014, growth in steel demand is expected to further accelerate to 7.0% thanks to the reform measures aimed at narrowing the fiscal deficit, coupled with measures to improve the foreign direct investment climate.

Steel demand in Japan is expected to decline for the second consecutive year in 2013 by -2.2% to 62.6 Mt due to contracting shipbuilding and automotive sectors despite a positive boost from the construction sector. In 2014, it is expected to contract again by -0.6%. This is due to an end of fiscal stimulus and structural factors, for example, increasing relocation of production by Japanese manufacturers overseas.

In 2013, in the US, after growth of 8.4% in 2012 due to the automotive and energy sectors and an increasingly resilient construction recovery, apparent steel use is forecast to grow by 2.7% to 99.3 Mt due to continuing fiscal concerns. In 2014, steel demand is expected to increase by 2.9%, thus exceeding 100 Mt with the help of positive momentum from the construction sector. For NAFTA as a whole, apparent steel use will grow by 2.9% and 3.0% in 2013 and 2014 respectively.

In Central and South America, apparent steel use is projected to rebound by 6.2% in 2013 to 49.8 Mt from 2.6% growth in 2012. The region’s steel demand is forecast to grow by 4.3% to 52.0 Mt in 2014. In Brazil, a rebound in investment coupled with the end of the recent de-stocking process is expected to bring apparent steel use growth of 4.3% to 26.2 Mt in 2013 and further growth of 3.8% to 27.2 Mt in 2014.

In EU27, the lingering uncertainties associated with the euro crisis continued to weigh heavily on economic activities in the region, especially during the last quarter of 2012. As a result, apparent steel use in 2012 fell by -9.3% with a widening gap seen at the country level. In particular, in Italy and Spain, apparent steel use contracted by over -18% in 2012. With signs of stabilisation in the economic situation, recovery is expected late 2013, but the economic prospects for the region remains weak. Steel demand in EU 27 is expected to contract further by -0.5% in 2013, but will return to growth of 3.3% in 2014 to reach 144.1 Mt.

Growth of apparent steel use in the CIS region is projected to slow to 2.0% reaching 57.6 Mt in 2013 as the modest pickup in Russia is partially mitigated by declining demand in Ukraine and Kazakhstan. In 2014, steel demand in the region is expected to grow by 3.8% to 59.8 Mt with the improving external environment. The resumption of energy projects and improving construction outlook is expected to support steel demand in Russia. It is forecast that steel demand in Russia will grow by 2.6% to 42.9 Mt in 2013 and will grow further by 3.9% to 44.6 Mt in 2014.

Steel demand in the MENA region is expected to grow by 3.2% to 65.2 Mt in 2013 after 2.2% growth in 2012 aided by reconstruction activities in the Arab Spring countries and Iraq as political turmoil in the region phases out. In 2014, steel demand in the region will further accelerate to 7.1% growth to reach 70 Mt supported by strong construction activities.

- The World Steel Association (worldsteel) is one of the largest and most dynamic industry associations in the world. worldsteel represents approximately 170 steel producers (including 16 of the world’s 20 largest steel companies), national and regional steel industry associations, and steel research institutes. worldsteel members represent around 85% of world steel production.

- The projections forecast by worldsteel consider both real and apparent steel use. Apparent steel use reflects the deliveries of steel to the marketplace from the domestic steel producers as well as from importers. This differs from real steel use, which takes into account steel delivered to or drawn from inventories.

- The Short Range Outlook is provided by the worldsteel Committee on Economic Studies which meets twice a year. The Committee membership consists of chief economists from more than 40 of the worldsteel member companies. The Committee considers country and regional demand estimates to compile a global overview on apparent steel use (ASU). The Short Range Outlook is presented to the Board for their final review before publication.