Globally, student housing is acknowledged as an important and lucrative real estate segment, generally included under ‘alternative’ real estate asset classes. In its current form in India, student housing essentially comprises of buildings that primarily offer residential accommodation for large numbers of students in boarding schools, colleges or universities. However, the residential facilities in such institutions are invariably severely under-equipped to match the demand for them. Also, the services and amenities they often fall far short of the international standards seen in established student housing markets such as the US or UK.

Globally, student housing is acknowledged as an important and lucrative real estate segment, generally included under ‘alternative’ real estate asset classes. In its current form in India, student housing essentially comprises of buildings that primarily offer residential accommodation for large numbers of students in boarding schools, colleges or universities. However, the residential facilities in such institutions are invariably severely under-equipped to match the demand for them. Also, the services and amenities they often fall far short of the international standards seen in established student housing markets such as the US or UK.

The education sector in India is growing rapidly. With the increasing number of students enrolling for higher education each year, student housing is obviously a complimentary product to this growth. Interestingly, the opportunity has come at a time when residential real estate (largest sector accounting for close to 85% of the value of investable real estate market) is currently slow and certain developers could bank on this opportunity to transform specific under-construction residential projects into student housing, bringing it under the more lucrative rental-yielding commercial project stream.

Emerging concepts like student housing can help developers and investors diversify into an income-yielding asset class that can potentially offer higher yields than the commercial office and retail properties because of a favorable demand-supply scenario.

In the US and UK markets, student housing is already an established and investor-friendly asset class because of its size and attractive market yield. Globally this segment, which has already attracted 200 billion dollars of investment, is essentially operated on a lease rental basis. Student housing in London has gained prominence mainly because of the higher yield rate, which has recently been 4.5% versus commercial yield rates of 3%.

Source: JLL

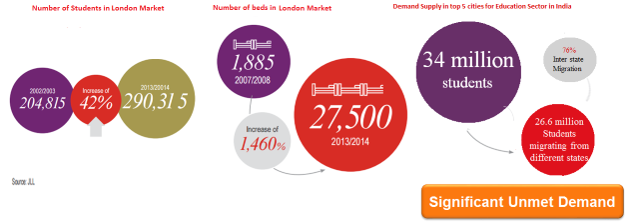

In London, there are currently 376,000 student enrolled for higher education, out of which 290,000 are full-time students. This number has grown by 42% in the 10-year period up to 2013-14 academic year as shown in the figure above. A significant 28% (104,000) of the total enrollments are from student outside the UK who need a local accommodation. This statistic has almost doubled in the said period. Globally, the number of students abroad is likely to double to 8 million by 2025 according to OECD ‘Education Indicators’ estimates, which also predict that London will have 224,000 students in the next decade.

Despite being an established market for student housing, the UK is also confounded by a demand-supply imbalance that works in favour of developers and investors in this asset class. The student housing market there has also evolved to a level where differentiated categories – premium (examples include brands like Nidos and Urbanest) and mid-level (Unite and Liberty) – have evolved. Both categories have been successful in the UK, and achieve high yield rates.

The potential for success of in the student housing real estate market in India could be similar or even more to that in the UK. Some of our cities, such as Pune, Bengaluru and Chennai, see very high annual student enrollments. There are 34 million students in India for higher education, of which 76% (26.6 million students) migrate from different states to these cities and invariably require accommodation. A broad estimate indicates that currently, cities like Pune and Bengaluru can only accommodate about 18-20% of the inward migrating students.

In short, student housing as a product is severely undersupplied in the major markets, and has the potential of high and sustained occupancy rates. This provides a marked opportunity for investors focused on attractive yield-based real estate products. Concurrently, student housing in India has immense scope to be developed as an asset class for developers.

It is true that this is a very new and therefore largely unfathomed asset class in India. However, so were malls and serviced apartments at one point in time – both products which have now successfully transitioned into organized sectors, and are moneymaking asset classes. The demand for student housing in India will continue unabated and in fact grow rapidly, so this is alternative real estate segment has all the hallmarks of becoming a revolutionary new product in Indian realty.