Ashutosh Limaye, Head – Research & REIS, Jones Lang LaSalle India

Ashutosh Limaye, Head – Research & REIS, Jones Lang LaSalle India

Recently, the RBI announced a measure that created ripples on the residential real estate market – the monetary authority sent out a warning to banks not to lend money to builders under the 80:20 or 75:25 schemes. The timing could not have been worse, coming as it did just before the festive season. This is a period in which consumer spending is generally higher, and developers often announce schemes that could help them sell high-priced apartments. 80:20 was one of such scheme, wherein the buyer agrees to pay 20% of the flat cost upfront. The remaining amount is funded by the bank after signing a tripartite agreement between all three parties at stake here.

The Impact

Several viewpoints have been floated since the RBI announced this ban, largely speculating on a fall in real estate prices as a consequence. It has been opined that developers’ holding power will be significantly reduce, forcing them to reduce prices. This analysis of the situation is based on the currently high levels of inventory that developers are saddled with, especially in larger cities like Mumbai, Bangalore and Delhi.

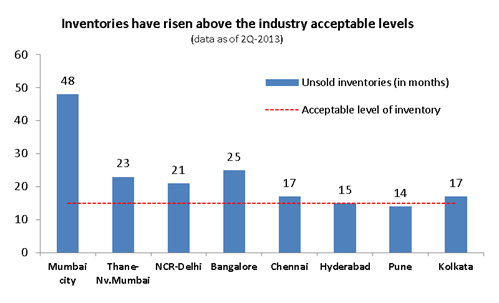

Indeed, inventory levels in the leading seven cities in India are much higher than the comfortable industry levels seen around 8-10 months ago, which is between 14-15 months’ worth of unsold supply:

(Source: JLL REIS)

Big City Real Estate Dynamics

Despite the RBI’s edict, it is important to note that there are dynamics at play in some of these larger cities which could result in developers resisting price cuts. In the first place, the cost of land in these cities is already at astronomic levels. Secondly, the recent amendment to the Land Acquisition and R&R Bill will raise land owners’ expectations, which means that developers will have to negotiate harder for available land. As a result, developers in these cities will now operate from the standpoint that overall real estate prices will, in fact, rise going forward.

Moreover, real-time appreciation in property prices (adjusted for inflation) in tier-1 cities during the last few years (1Q12-current) have not more exceeded 4-5% – a fact that could dissuade developers from reducing property prices significantly. It is also pertinent to note that most projects within the municipal limits of cities like Mumbai, Delhi and Bangalore these cities are targeted at HNIs / NRIs, who can afford to purchase these properties without availing of bank funding.

Significantly, a large number of projects that are completed or under-construction is in the high-end segment, which in any case places them out of reach for mid-income buyers. Therefore, a marginal price correction in these apartments would not augment demand from the non-affluent class.

Short-Term Correction?

While these are enough reasons for developer to hold their prices at the current levels, a marginal correction in the prices of certain projects aimed at the mid-income segment is not entirely out of the question. If it occurs, it would be within a range of 12-18%, depending on specific projects and their builders’ holding capacity and financial strength. A correction in prices beyond this level would affect developers’ profitability to a non-acceptable extent.

Any discounts that we see this festive season will be a function of developers’ need to sail through the current difficult market conditions. With the slightest indication of a recovery in economy, this window of opportunity will close, as has been amply evidenced in the past.

Much of the uncertainty surrounding the Indian economy currently revolves around the global market conditions, and also the doldrums that most markets experience prior to general elections. Depending on the new policies that invariably define the post-election scenario in India, there could be a major change in the country’s economic status quo, which will automatically reflect in market sentiments.