Anuj Puri, Chairman & Country Head, JLL India

Anuj Puri, Chairman & Country Head, JLL India

The monetary policy announced today indicates that the RBI is of keeping a close eye on inflation rather than facilitating growth just as yet. This makes sense. Globally, emerging markets (including India) continue to remain vulnerable from decisions by US Federal government on withdrawal of stimulus, as well as geopolitical tension in the Middle East – which could impact crude oil prices.

In India, leading indicators such as the monthly Industrial Production and Purchasing Managers’ Index (PMI) have provided early signals of strengthening corporate sales and business flows. The benign outlook on global non-oil commodity prices and still-subdued corporate pricing power should all support continued disinflation, as should the recent government measures to improve food management.

However, the RBI has deemed it premature to conclude that future food inflation and its effects on broader inflation can be discounted. Also, the government is currently constrained by high deficit and its ability to spend is therefore restricted.

This actually opens up space for banks to increase lending to the private sector. Thus, there is a need to increase liquidity with banks in order to enable them to meet the additional financing requirements.

Key Policy Changes

- In line with the street estimate, the RBI has kept the benchmark interest rate (repo rate) unchanged at 8.0%. All other key policy rates, barring SLR, also remain unchanged.

- The statutory liquidity ratio (SLR) of scheduled commercial banks has been reduced by 50 basis points from 22.5 per cent to 22.0 per cent, thereby increasing funds available with banks for lending to the private sector.

Impact On The Real Estate Sector

In line with the recent initiatives of the government as well as the RBI to push for growth in infrastructure and real estate – specifically affordable housing – the additional funds allocated in the hands of commercial banks through a SLR cut is positive for both these sectors. The investment cycle is picking up, as is evidenced by the recent Index of Industrial Production (IIP) and Purchasing Managers’ Index (PMI) numbers. Therefore, banks’ willingness to lend the excess liquidity generated to these priority sectors is likely to be high. As far as interest rates are concerned, the real estate sector will have to wait a little longer for a rate cut.

Generalised inflation and interest rates are just one aspect of the costs incurred by developers in India. The other major aspect is construction cost, which has been rising at around 17% year on year for last 4-5 years. The reason for this imbalance is largely the supply-side constraints. It is important for the RBI and the government to cohesively work towards clearing this demand-supply imbalance. The signals coming from the monetary and fiscal authorities are currently positive. To that extent, the real estate sector certainly has reason to look forward with enthusiasm.

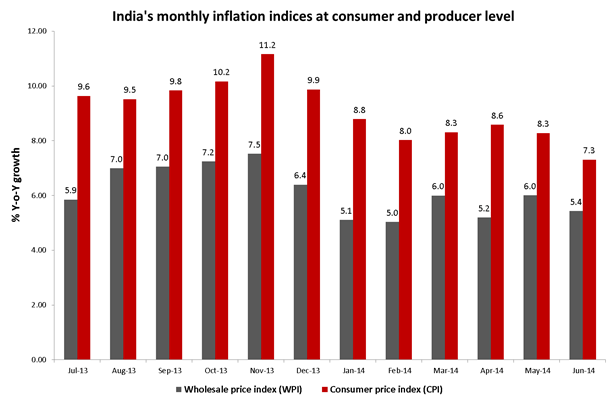

Current Inflation Scenario In India

Over the last three months, CPI inflation (a number that RBI closely follows) has moderated. As of June 2014, it stood at 7.3% y/y, giving some comfort to RBI. The RBI could have lowered its hawkish tone and reduced interest rates marginally at this point, but the deficit in monsoon and a yet-to-reflect impact of the recent hike in rail ticket prices are potential threats. Therefore, lowering its guard against the inflation threat would have been premature.