Anuj Puri, Chairman & Country Head, JLL India

Anuj Puri, Chairman & Country Head, JLL India

The year 2014 has been quite fruitful for the real estate sector in terms of business sentiment, although the real effect of many of the policies and amendments announced in 2014 will take effect only in 2015. Starting from Union Budget FY2014-15, where affordable housing was considered on par with infrastructure, to relaxation of rigidities in the Land Acquisition and Real Estate Regulatory Bill, India’s new Prime Minister has been offering the India real estate sector consistent doses of energy.

The winds of change are now blowing more perceptibly. Inflation, including the house price component, has now been reduced to the lowest level in recallable history. Property buyers are back in force in most cities as enquiries have rebounded, and developers are finally reading the writing on the wall more accurately and coming in with the kind of supply that is relevant to demand.

Meanwhile multinationals that were hesitant to foray into the Indian market because of the uninspiring political environment are now dusting off their plans for India and getting their entry vehicles back in gear. Going by the recent reports of recruitment agencies, many more jobs will be created in 2015 – especially in the IT/ITeS, manufacturing and services sectors – and the demand for homes will increase visibly. Also, REITs are hitting the market at long last, and only a few details need to be sorted out before they get the funding wheels spinning.

2015 will definitely be a good year for the real estate sector on three counts:

- The threat of inflation has completely submerged, and borrowing rates are sure to go down from the current levels. This will encourage potential buyers planning to avail of home loans to finally take the plunge. Also, with property prices staying stable and good deals being offered by developers in order to clear their inventory, fence-sitting buyers be further encouraged to press the ‘buy’ button.

- Economic activity is gradually picking up, and the Central Bank anticipates GDP growth to reach 6.5% y/y in the next financial year (FY2015-16). Corporate India has already made it clear that there will be more hiring of talent to help tackle rising business activity. Put together, this means a rise in jobs and incomes, which in turn is very favourable for both residential and commercial real estate.

- The market has witnessed a re-orientation and developers are now largely focusing on affordable homes. This will go a long way, though definitely not all the way, in bridging the existing wide gap between demand and supply of affordable homes.

Residential Real Estate

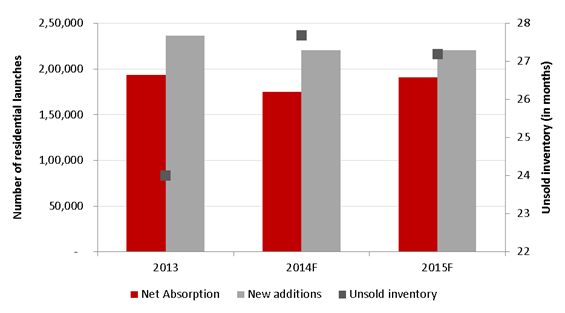

During the year 2014, new launches of residential units saw a consistent fall every quarter as a consequence of the subdued demand and high prices. While this was largely the case with high-end projects, the affordable housing segment definitely began to gain favour. This segment was firmly lodged under the priority schemes of the government and central bank, and buyers were seen finding comfort in investing in such projects given the smaller ticket sizes and improving connectivity in the suburbs of the major cities.

In the second half of 2014, many large developers who in the recent past concentrated on the mid-to-high segment due to better margins were seen eager to play the volume game and entering into affordable-segment projects in the deeper suburbs. This heartening trend began the ground work on bridging the wedge between demand and supply in our major metropolitan cities. Since developers are sitting on close to 30 months of unsold inventory in the mid-to-high-end segment, we also saw an increase in cash flows because of this new focus.

Completions, Net Absorption & Unsold Inventory – Residential

In 2015, developers will become more earnest about right-sizing and right-pricing their offerings. Smaller, yet better-designed and more efficient homes will define the residential real estate market in 2015, and selective corrections in some of the over-priced cities will help bring about faster sales for stagnated supply of larger configurations. Townships will become more prevalent, and the supply of luxury homes will moderate to align with the slow demand dynamics for these offerings.

- Pricing Trends

A large portion of the total unsold residential inventory is in the under-construction projects, while completed projects have only moderate vacancy. Home buyers looking for ready-possession property will therefore find limited room for negotiations when compared to buyers who can wait for some time to get possession. The attractive schemes that were doled out by developers in under-construction projects during the festive season of 2014 are likely to continue into 2015.

2015 will see home buyers benefiting from reduced borrowing rates, increased developer-focus on affordable homes, largely stable prices, and better job and income prospects.

- Affordable Housing

Affordable housing will clearly be the flavour of the season in 2015. While the ruling government at the Centre and the Central Bank have clearly spelled out their intention to push for affordable housing, it is the State governments which will need to take the implementation initiative. The recently concluded elections have clearly indicated that better governance, planning and good implementation are factors on which performance will be evaluated, and affordable housing is an important yardstick for sure.

While affordability will always be a subjective term that assumes different meanings in different markets of India, every city does have its own affordability threshold and benchmark. Developers active in each of the primary cities are now fully aware that they must address the demand for affordable housing in their cities, and stop focusing excessively on high-end and luxury offerings.

Affordable housing is in itself not a difficult format to deliver; the challenging part for many developers will be to align this format with their existing brand image without impacting it. Quite a few prominent developers already have a budget housing strategy, but they have evolved this strategy over time and ensured that the creation of such projects becomes a natural extension of their brands. For the newer entrants who have so far focused exclusively on higher-end housing, the process will begin only now – and for all but the die-hard firms that will not budge from their ‘creamy layer’ orientation, the process is unavoidable.

Coming anywhere close to negating the affordable housing gap altogether would take about two decades of focussed supply – and going by previous market learnings, it is unlikely that developers will retain their current focus on affordable housing once the economy picks up sufficiently to make higher-end housing desirable once again. However, as long as the current momentum and orientation prevails, we will at least see some good headway being made on this front in 2015.

Commercial Real Estate

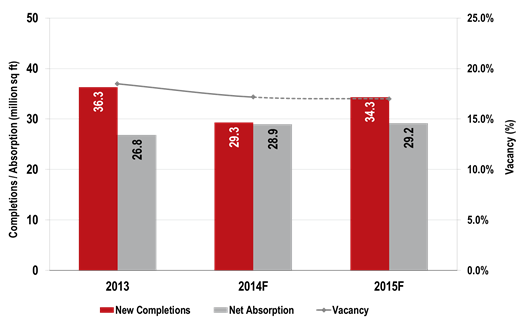

Over the past few years until 2014, the supply of office real estate was higher than demand by 4 to 10 million sq ft. Our reading is that developer had been too optimistic in their anticipation of a revival in economic activity.

Though office real estate prices failed to recover from the after-effects of the financial crisis up to late 2014, we did see the beginning of a gradual turnaround. This can be attributed to the fact that commercial real estate developers began to strategically reduce the incoming supply to a new-normal level of occupier demand in the range of 27 to 30 million sq. ft. each year. This helped bring down the vacancy rate to 17% from more than 18.5% just a year ago.

In 2015, demand will remain in this range, marginally improving from the level seen in 2014. However, with the rupee weakening to below INR 62/USD at the current time and India’s GDP growth likely to strengthen further, the positive risk to this forecast of a sharp uptick in demand cannot be ruled out though.

Interestingly, while office real estate have not recovered fully from the fall in prices post GFC (unlike residential) there is significant room for upside in the event of a positive change in business sentiment. In fact, such an improvement was already seen after the general elections and is already reflecting in year-end office market leases. The trend of moderate-to-healthy leasing activity will continue in 2015.

Pan-India New Completions, Absorptions and Vacancy – Office

Retail Real Estate

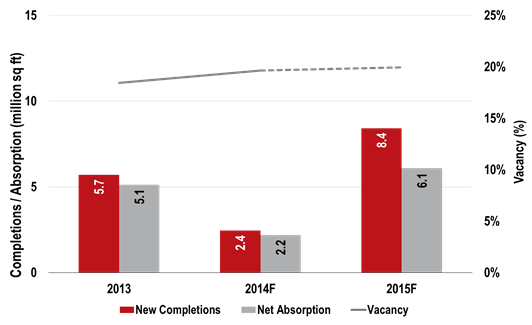

In 2014, the retail real estate sector was one of the biggest casualties to market conditions that increasingly favoured the online retail community, with the exclusion of well-managed and leasehold organised retail malls. Strata-sold, poorly-managed, badly-located retail properties lost lustre as more retailers chose to avoid them.

2014 also saw a few of these malls either converting into Grade B office space or reeling under the compounding effect of rising vacancy rates. Vacancy in poorly-built and operated malls was as high as 20%, while good quality malls were relatively better off with about 10% of vacant space. The ecommerce frenzy that has been taking India by storm over the last two years was at its peak during 2014, and now poses a serious challenge to physical retailers and mall developers. The situation is compounded by the absence of adequate regulation on ecommerce in India currently.

However, a handful of mall developers have risen to this challenge by identifying key transitions that could help them sail through. The measures they have undertaken include a revamped tenant mix, adoption of the mixed-use format and delivering theme-based shopping experiences. These practices are now common in overseas markets, and Indian retail malls will be seen adapting to them more rapidly in 2015.

Pan-India New Completions, Absorptions and Vacancy – Retail

Real Estate Capital Markets

2014 saw gradual growth in demand for Indian real estate, particularly after the general elections in May. Concurrently, fund raising activities picked up, and this momentum will continue in 2015 as well. We will see less of one-way investments and more of partnerships between investors and developers and other land owners.

Joint venture and club funding will become the preferred mode as 2015 progresses. With the improvement of the economic situation, Pune, Chennai, Hyderabad and Kolkata will start attracting sizeable investments along with the top three metros of Mumbai, NCR and Bangalore. This will be a notable change from dynamics seen in the past, wherein only these three cities ruled the roost. In fact, we will see Grade A commercial properties in tier 2 and tier 3 cities appear on the radar of investors, though a full-on focus on these opportunities will probably not take place in 2015.

Attractively-placed office assets and high-demand residential categories, especially well-located mid-income projects, will continue seeing considerable investments in 2015.While investors may continue to show limited interest in retail real estate, we will see increased interest in the hospitality sector as compared to previous year.

REITs got a green signal from the government in 2014, and this will help ease the pressure on the balance sheets of cash-starved developers. However, the listing of new REITs will be slow and steady. While REITs will succeed over the longer term, they need to pass through the challenging phase ahead for them over the next two years.

Real Estate Regulation

On the regulatory front, Indian real estate will continue to faces a fair share of problems in 2015.There are currently still a number of vital regulations and initiatives related to real estate that have been gathering dust on bureaucratic tables. These need to be fast-tracked and implemented in 2015, because they are crucial for the real estate sector’s growth and graduation from opaqueness to transparency.

While many believe that there is little done by the currently ruling government for the real estate sector, there is a positive sentiment underway owing to small but significant steps taken in the right direction by the new government.

In the recent past, two landmark policies that were introduced by the central government were the Land Acquisition, Redevelopment and Rehabilitation (LARR) Bill and the Real Estate Regulatory Authority (RERA – yet to be ratified). However, after almost a year of these two bills being introduced, there has not been much progress. This is largely due to tough clauses included in both these bills, which were actively debated throughout 2014. Some of those clauses were seen as limiting the ability of the industry to function smoothly.

The newly-elected government has astutely identified the limiting factors within the two bills and attempted to rectify them rather than introduce new regulations that would merely add to the burden of ‘lip-service’ reforms. In that sense, the present government has done its homework before taking up the task of resolving issues of the real estate sector.

Once finalised, the revised bills will appear more investor-friendly and create a favourable environment for developers, buyers, and investors to operate in 2015as the key changes mooted in the two bills are:

– Land Acquisition, Rehabilitation and Resettlement Act (LARR)

The single-biggest hurdle that the entire real estate sector will face in 2015 is related to land – the very foundation stone of all real estate. The finite and all important commodity of land is caught in a regulatory stranglehold that we hope to finally see loosened in 2015 – especially given the incumbent government’s vision of establishing 100 Smart Cities, which gives rise to serious questions about feasibility. The creation of these 100 smart cities will entail significant volumes of land – massive, contiguous land parcels.

In the manner that the new government has envisaged, these smart cities will essentially be brand-new municipalities on the peripheries of our major cities. With its avowed commitment of launching 100 smart cities, the government is de facto also making itself responsible for making the required land available. How exactly will this happen?

The LARR (Land Acquisition, Rehabilitation and Resettlement) Act was formulated and re-formulated to counter land-related bureaucracy in India. On the ground, it has actually done quite the opposite ad become a deterrent for developers as well as investors to operate in the Indian real estate and infrastructure space.

The real estate sector is desperate to get past this hurdle. It is not just a question of making land available for primary real estate development; the government has correctly identified infrastructure development as they key to accelerated economic growth, and infrastructure is highly land-centric.

The modified LARR Act which was put into effect last year by the UPA government attempted to reduce the bureaucracy involved. However, it failed to achieve this purpose and in fact only increased the existing complexities. Given the new government’s sharp focus on ‘housing for all’, fast-tracking of infrastructure and the creation of 100 smart cities across the country, there is very clearly a pressing need to revisit this Act in 2015. Provisions in the bill such as the significant rise in compensation to original inhabitants, the tedious rehabilitation clauses and other norms need to be relaxed if it is to serve its purpose of untangling complexities and delivering a fair shake to all stakeholders.

- Consent clause: The current legislation requires the acquisition process to go through mandatory consent of at least 70% locals for PPP projects and 80% consent for private projects. This clause is difficult to implement, considering the large number of people involved in the entire rehabilitation process. The fact that the government is planning to renegotiate these clauses is in itself a big positive, as one tight spot has been identified.

- Return of unutilised land: It has often been seen that when land was acquired for a stated purpose and the land-losers were promised employment opportunities and overall development of the region in question, the project failed to take off for several years. This lacuna has been identified, and the timeframe for return of unutilised land has been proposed to be reduced to 5 years from the previous 10 years. This is a strong deterrent for companies or developers who plan to acquire land without having a clear roadmap for its usage.

- Clarity on end-usage: There is a need to clearly identify the purpose of land acquisition so that intervention by the government can be put to right use. For instance, critical projects involving infrastructure and affordable housing require faster clearances and may necessitate timely intervention.

- Expertise of State governments in deciding area threshold: The amended Land Acquisition Act was to cover all private land acquisitions if the minimum area to be acquired was 100 acres in rural areas and 40 acres in urban areas. However, every city and village has different dynamics, and these are best understood by the State government rather than the Centre. Thus, the Act must consider giving States an upper hand in deciding the coverage reveals pragmatism and flexibility.

- Smart Cities beyond PPP: In order to meet the target of an annual outlay of INR 35,000 crores for development of 100 new smart cities, it was obvious that private funding was critical. The government has invited full private funding of projects, with government contribution largely limited to viability gap support.

– Real Estate Regulatory Bill (RERA)

The still-pending Real Estate Regulatory Bill has been hotly contested at every stage, and its approval has been deferred once again only recently. There is no doubt that it must be enacted sooner rather than later so that the Indian real estate market becomes attractive for foreign investors. However, no version of this Bill that has evolved from the various objections and arguments from the industry’s stakeholders has been universally acceptable so far. It will require a strong and determined government to push it through.

Three recent revisions to the RERA could conceivably lead to its unilateral acceptance and consequent ratification in 2015:

- Reduction of minimum balance to be maintained in the escrow account of a project has been reduced from 70% to 50%: This amount was from the monies collected from the buyers. This will effectively allow developers to continue their practice of diverting funds collected for a project towards land acquisition or other projects, and will work in their favour by also allowing them to grow their land and/or project portfolio. The 50% mandate will still place enough restriction on developers to divert funds elsewhere and ensure better completion records. (However, for buyers, the concerns regarding funds diversion would be higher, and the Bill would be slightly less protectionist towards buyers.)

- Coverage expanded to the commercial real estate sector: While the previous version of the bill envisaged coverage of only residential sector, the new government wants commercial real estate to also fall under the ambit of the regulatory authority and its clauses. The limited coverage was largely without any purpose and, therefore, it currently stands rectified. Commercial projects under the purview of the bill would provide protection to investors of commercial assets, as well.

- All projects which have not received their completion certificates will also be now covered under the bill and hence this allows larger umbrella coverage for buyers and investors.

Worryingly, while the RERA initially aimed at providing an alternate redressal mechanism, the new provisions are talking of no recourse to other consumer forums. This can lead to pressure on this regulatory body in terms of increases log of cases, though it will reduce instances of multiplicity of suits.

In any case, the recommendations have been made by the ministry and sent to PMO for approval before the cabinet approves it. Thereafter, it will be tabled in the Parliament for passing the bill and making it an act. It is unclear whether the Real Estate Regulatory Authority will finally be ratified as a law in 2015, but the fact that hard discussions are happening is definitely positive, and indicative of the new government’s determination to make it a reality.