Delhi in top 15 markets, Bengaluru and Chennai in top-25 markets

Ramesh Nair, CEO & Country Head, JLL India

Even as a number of Asia Pacific markets – led by Australia – showed improvements to gross leasing volumes, overall regional volume was held back by India where markets cooled as supply volumes dropped sharply. In aggregate Asia Pacific, gross leasing activity was down a modest 4% y-o-y. Broad-based demand underpinned strong growth in Australia. Greater China and Southeast Asia also registered healthy growth.

Melbourne registered some of the strongest growth in the region while Shanghai volumes picked up on the back of solid leasing activity at recent completions. IT/ ITeS, manufacturing and professional services firms contributed to solid growth in Delhi volumes. Bengaluru registered the sharpest fall in leasing volumes as activity was circumscribed by tight vacancy. Overall, financials and tech firms remained the key drivers of office leasing demand.

Asia Pacific rent growth accelerates

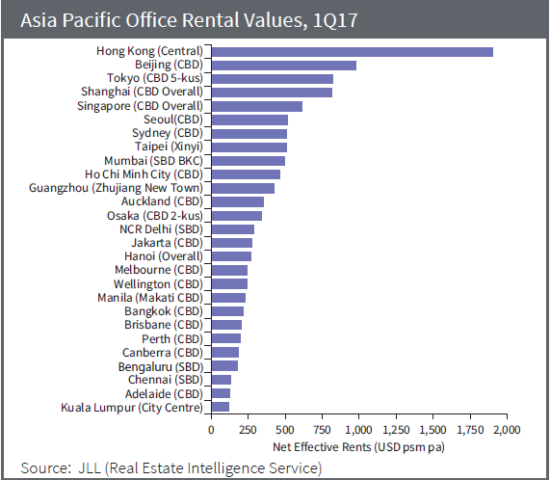

Asia Pacific office rents increased 1.0% q-o-q (2.9% y-o-y), slightly faster than the 0.7% q-o-q (2.3% y-o-y) growth registered in 4Q16. In 1Q17, Mumbai figures in the top-10 markets with highest office rental values across APAC, which is led by the priciest market of the region – Hong Kong – and also has cities like Beijing, Tokyo, Shanghai, Singapore, Seoul and Sydney.

Delhi sits in the top-15 markets just trailing Osaka and Auckland. Bengaluru and Chennai both sit in the top-25 markets with their rents only higher than Adelaide and Kuala Lumpur. Among these four markets, only Delhi recorded negative q-o-q as well as y-o-y rental growth. Rents of either the central or secondary business districts were considered for each in this index, on a net lettable area basis.

Sustained acceleration seen in capital value growth

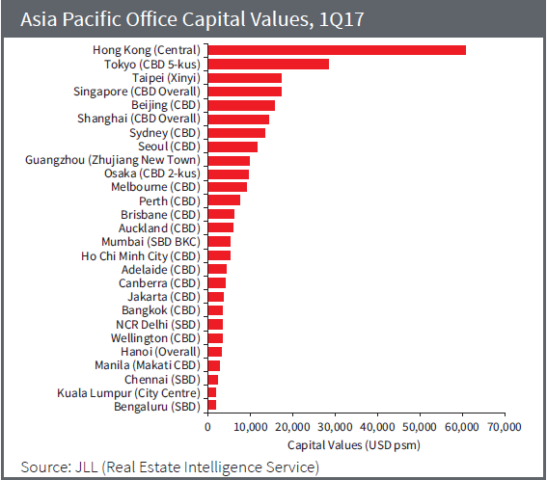

Largely supported by the increase in rents, capital value growth accelerated to 1.8% q-o-q (4.9% y-o-y). In 1Q17, Mumbai sits among the top-15 markets trailing Auckland and Chinese, Australian cities. Delhi-NCR, Chennai and Bengaluru all saw a more plateaued capital value growth and sit outside the top-20 APAC markets.

Rent and capital value growth to slow in 2017

Full-year 2017 Asia Pacific leasing volumes are expected to be consistent with 2016 levels. While occupier demand is expected to remain stable, a larger supply pipeline scheduled for 2017 is set to slow rent growth to 1-2% y-o-y. Sydney is still forecast to be the top performing market in 2017. Asia Pacific aggregate capital value growth is also expected to slow in 2017. Core yields remain at or near historical lows although there may be room for slight compression in some markets. However, the weight of capital chasing commercial real estate, particularly in major investment destinations, in combination with moderate rent growth is forecast to drive aggregate capital value growth of 2-3% in 2017.